In this episode we look at some of your questions and then take a look at the causes of Third World Debt.

Click here to view it in your browser or 'Right Click' and choose 'Save As' to download it without iTunes (208Mb).

Welcome to Money Myths Episode 4 – Q&A and Third World Debt

My name is Brian Leslie and I'm the editor of Sustainable Economics magazine.

Before we get started, I have a few things to mention.

This is part four of the series. If you haven't seen the Series Introduction and parts 1 to 3, I would suggest that you watch them first, in order, as we aim to build the series on the basis that viewers have seen these episodes.

The other episodes are available through the rss feed or the site that you downloaded this episode from. They are also available through our website (www.moneymyths.org.uk). Please visit the site, where you will find information about the series, a list of episodes, links to further information and details of how to contact us to ask questions or make comments.

There is a "Subscribe to the Series" link, to subscribe via iTunes or Miro to get all the episodes as they become available, as well as full transcripts of each show and any relevant links to other information.

We very much appreciate getting your feedback and questions, some of which will be answered in this episode. Other questions will be answered in a later episode. Please keep sending your questions to us via the email address on the web site.

Although we are not aiming to make a profit from this series, we do have expenses that have to be covered. You’ll find a "Donations" button, if you’d like to contribute.

As in previous episodes, I am referring to the British Banking System for this series. However, the system in most countries is the same and has a similar history. I leave it up to you to substitute your own Central Bank, Government, Ruler, and so on.

As I promised in the last episode I will now answer some of the questions that people have asked so far. I will then go on to look at the causes of the ‘third world’ debt problems.

I have picked the five questions that have been asked the most.

Q1. Now that I understand the problem, what can I do about it?

There are several possible answers to this question.

First, talk to your friends and family about the issues. Get them to watch the series. Look at other web sites on the subject. (Some links are on our site).

Second, write letters to your MP, the Chancellor of the Exchequer and your local papers. Try to get some discussion going at work.

Third, get involved with local political groups, whether mainstream or alternative and bring these ideas to their notice.

Fourth, make copies of the series on CD or DVD or print copies of my booklet, Where’s the Money to Come From??, and offer them to your local schools, colleges and local libraries. The booklet is available on the ‘links’ page of the web site. Copies are also available from my other site, for a small fee, at www.sustecweb.co.uk.

Fifth, challenge the Government to clarify what it means by the 'quantitative easing' it is thinking of introducing. This appears to be a way to conceal the fact that it would itself be creating and spending at least some book-entry money, as monetary reformers have been urging, but using it for the wrong purposes! (So far, I have not gained a clear, factual answer to this. Let me know if you succeed in getting one.)

Q2. “Let’s hope we end up back on a Gold standard with no inflation or expansion”.

This is often proposed by people who are opposed to usury. The problem with gold (apart from the environmental and human cost of extracting it from Nature) is that the amount available does not reflect the need of society for a medium of exchange. It can be almost guaranteed there would be either too much or too little.

What is needed is a more adjustable supply. This is what fractional-reserve banking provided, and is the basis for its success – so far. But, as I have outlined, it has many serious ‘downsides’, especially in creating growing debt and inequality.

As I have already argued, the simple alternative is to use book-entry money, but to spend it into circulation. This requires a State body charged with maintaining the supply at the level required. It would be required to determine this amount over time. It would adjust the amount by crediting the Treasury’s account, for the Government to spend into circulation, or if there is ever an excess, to demand repayment to it from the Treasury, for cancellation.

Q3. Why don’t we repeat the important points?

We try to keep each episode fairly short & keep the size of the files as small as possible. We try to avoid repetition as you can always go back and re-watch any episode or you can look on the web site to get the show’s transcript and read it at your leisure.

Q4. Why is this series being done as a video?

We decided to produce this as a video, rather than as an audio series because of the graphs that need to be understood. We did consider both formats and, as most people in our target audience have broadband, we decided that video would be the best format.

Q5. I'm never content with just watching a one-sided presentation of ideas like this – which economists are your critics and what do they say?

I don’t understand the point of this question. I am presenting my ideas, based on years of research. It is not up to me to list people who disagree with me. Did Galileo list the members of the church who disagreed with him? Does that make his ideas any less valid? For alternative views, I would suggest reading any of the course materials for current mainstream economics qualifications.

I hope that answers these questions.

Now on to the next main topic: ‘Third World Debt’.

In the last episode, I noted that speculation – gambling – on the foreign exchange markets now involves well over twenty times the amount of money used in the international trade in goods and services. This is made possible by huge short-term loans of bank-created credit, especially since the bank-deregulation of the 1980s.

This speculation would hardly be possible except on a very small scale, if banks were suitably regulated and entirely denied the privilege of money creation. This gambling seriously distorts the exchange rates, and commonly works to the disadvantage of ‘third world’ debtor countries.

Another factor in the growth of ‘third world’ debt is the huge loans these countries were persuaded to take on, really to profit the lenders – the western, mainly US, banks.

These loans happened mainly as a result of the oil ‘price-hike’ of the OPEC countries in the early 1970s, the profits from which were deposited largely in US banks.

This money enlarged the banks’ reserve base and so encouraged them make further, profitable loans, using any opportunity to fund projects in the developing nations. They were not concerned about how unethical they might be. Profit was their only motive.

The theory was that the loans would be invested in projects that would enable these countries to produce export goods to create profits to pay off the loans and leave a surplus – but this rarely happened.

In some cases, corrupt leaders received these loans, but many other loans were simply unrealistic. Lenders, in their rush to make loans, made mistakes. They promoted projects without serious consideration of the prospects of repayment. To encourage borrowing, the early loans were initially at fairly low interest-rates.

These loans were mainly made in the lenders’ currencies, mainly US dollars, not in the borrowers’ own currencies. Many loans had conditions that involved using materials and construction firms of the lenders’ countries. So that much of the money returned to the lenders’ countries without benefit to the borrowers.

Additionally, unfair terms of trade made it difficult for developing economies to export manufactured goods. Raw materials and agricultural products were encouraged – in competition with other developing countries, thereby driving down the prices they could obtain.

In the 1970s and later, the interest rates on these debts were greatly increased. This made debt repayment impossible.

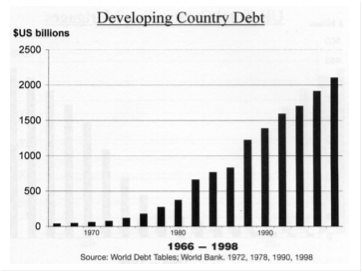

This graph shows the increase of Developing Country Debt between 1966 and 1998. You can see how the amount of debt increased greatly during the 1970s and since.

Banks charge compound interest on loans. As Wikipedia puts it, “Compound interest is the concept of adding accumulated interest back to the principal, so that interest is earned on interest from that moment on”.

Therefore, if a debtor gets into arrears, interest is then charged on the interest that they didn’t pay!

The growing compound-interest debt has meant that further loans became needed, simply to pay the outstanding interest on the existing loans.

The International Monetary Fund (IMF) and the World Bank, made many of these loans directly or they passed them on from commercial banks. ‘Structural adjustment programmes’ were imposed on the borrowing countries, as loan conditions, to boost export earnings. These conditions restricted expenditure on infrastructure, health and education. This worked strongly against the interests of the poor in those countries.

The charging of interest – usury – has been condemned over millennia as unethical and destructive of society. It used to be forbidden by the Christian Church, and still is in Muslim countries. According to the New Testament, Jesus threw the moneylenders out of the temple for the crime of usury!

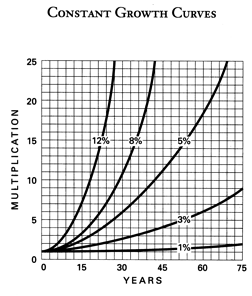

Compound interest, by its very nature, grows exponentially.

This graph shows how compound interest increases the total debt over time, assuming repayments are not being made.

It shows that, for instance, at 12% per annum, it will double the total in about six years, but multiply it twenty five-fold in only about twentyseven years.

At 3%, it would double in about 23 years, and multiply it three-fold in only about another thirteen years.

For any given rate, the longer it lasts, the faster it grows.

When our money supply depends almost entirely on compound-interest-bearing loans, we should not be surprised to find that debts are growing exponentially!

As Kenneth Boulding, an economist said, “Anyone who believes exponential growth can go on forever in a finite world is either a madman or an economist”.

Exponential growth can’t continue indefinitely. All around the world, debts of all kinds – personal, business and national – are growing in this way. This is the fundamental cause of the current Global Financial Crisis.

If we achieve the reform of the system as I have been recommending, so that our whole supply of national money comes into circulation by the Government creating and spending it, instead of allowing banks to create it as interest-bearing loans owed to them, this would eliminate the major cause of debt, and so, the major cause of the growth of debt.

This reform could be adopted throughout the world. A growing movement is demanding cancellation of ‘third world’ debts, and a small start has been made on doing it; but this challenges the basis of the present system of money creation.

Official acknowledgement of the need for the reform I am advocating would make a new start possible, globally. Then each country would have charge of its own currency, and could fund its own productive potential for the benefit, primarily, of its own people, exchanging abroad any surplus product, for the goods it needed.

Countries blessed with more than adequate resources for their own population should then be able and willing to gift-aid those less well-endowed.

The G-20 is the group of leaders from 19 of the largest national economies in the world plus the European Union. They are to meet under the chairmanship of Gordon Brown, the UK Prime Minister, in London, in April.

They will be debating possible solutions to the ‘credit crunch’. A proposal for national and international monetary reform on the lines I recommend has been submitted to the House of Commons Parliamentary Select Committee on the Treasury, which will be advising Gordon Brown.

Write to your MP to urge him or her to press for Gordon Brown to demand fundamental monetary reform!

In the next episode I will be looking a bit more at how the present system developed, against strong opposition, and at some successful breaks from it.